Beginning the process of planning your retirement may involve the following:

• Reviewing your current situation;

• Exploring strategies to increase your savings;

• Understanding the benefits that superannuation can provide; and

• Ensuring that your family is cared for – no matter what.

We have developed the following resource as an introduction and simple summary of the retirement planning process:

Doctor Rimmer’s Financial Health Guide

If you would like to understand the process in more detail, we have published Retirease, as featured on Amazon and available to purchase here.

This is a tough call, as the answer depends on a whole range of issues that boil down to where, how well and for how long you intend to live. Not always easy to answer in advance.

However, in an attempt to provide some clarity around the issue, we have developed the following resource:

For more information, we have published Retirease, as featured on Amazon and available to purchase here.

Under normal circumstances, superannuation does not automatically form part of your Estate, which could leave the decision as to the distribution of your benefit in the hands of the Fund’s Trustee.

An important part of your Estate Planning should involve lodging a Binding Death Benefit Nomination with your superannuation fund. This directs the Trustee of the Fund as to whom you would like your benefit to be distributed in the event that you pass away.

As the name suggests, so long as a valid nomination has been provided at the time of your death, the nomination is legally binding on the Trustees of the fund – that is, they must adhere to the instruction as set out in the nomination when distributing your benefit.

Depending on your fund, this nomination may be in the form of a lapsing or non-lapsing instruction.

Where the former is concerned, the nomination is valid for three years only, meaning that regular review is important.

Note, however, that choosing to make a non-lapsing nomination instead is not necessarily bullet-proof. Should your circumstances change (be it as a result of divorce, death, etc.), the nomination will still need to be reviewed and updated as a matter of importance.

For more information you can take a look at the following article:

For further detail, we have published Retirease, as featured on Amazon and available to purchase here.

ARA holds its own Australian Financial Services Licence No. 224150.

1. Initial service

The following outlines our advice process and any associated costs:

- Step one: We gather all the necessary information we’ll need to prepare a financial plan for you. Not just the numbers, but also an understanding of what you want to achieve from the exercise.

- Step two: We take that information away and prepare a strategic plan – a step-by-step action list of the things we recommend you do, and why.

- Step three: We get together again and take you through that plan. We use this opportunity to tweak it if necessary, until you’re completely happy with it.

- Step four: Once the plan is finalised, we formally document it for you in a Statement of Advice (SoA).

Our fee for this service is $1,595 (including GST). Any costs that might be incurred for future services will be outlined in the Statement of Advice, without any further obligation on your part.

2. Ongoing advice and services

Clients of ARA can choose to take up our Personal Advice Package to help them stay on track to meet their goals.

The service is available to individuals and couples whose primary need is continual oversight of their file and circumstances to ensure their portfolio of investments and strategies continue to meet their goals and aspirations.

The cost of this service (including GST) is:

- Monthly fee of $165; or

- $1,880 per annum if paid in advance.

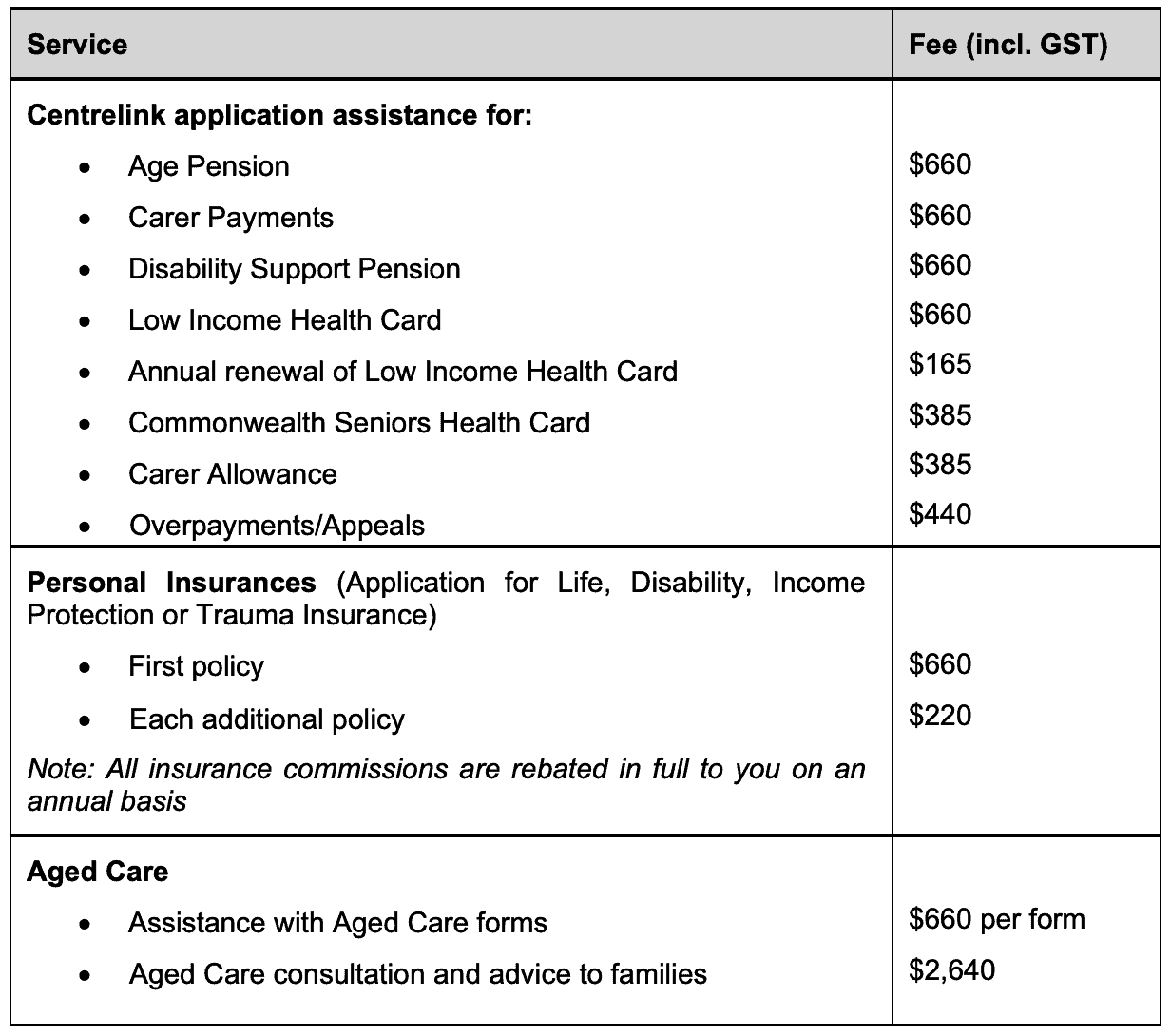

3. Fees for specific services

In addition to the Personal Advice Package, additional fees will apply if any of the following specific services are requested – as set out below:

4. Fees for additional or ad hoc services

For those that choose not to subscribe to the Personal Advice Package, clients of ARA can still access the expertise of our Advisers by requesting additional or ad hoc services on demand via a ‘pay-as-you-go’ arrangement.

If an additional or ad hoc service or transaction is requested, the fee is agreed prior to the additional service or transaction being executed.

Portfolio management services

Portfolio management services are usually provided by way of proprietary investment products which we have developed for the exclusive use of ARA clients. The products have no entry, exit or transaction costs or commissions payable. The annual management fee, deducted prior to the crediting of your return and which varies according to the portfolio selected, covers all of ARA’s costs.

Investor security is catered for in the following ways:

In conjunction with your ARA planner you get to choose an investment portfolio mix that suits your own needs and preferences. We can provide detailed illustrations that describe the likely range of possible outcomes you can expect from your investment and the risks you are taking. Furthermore, ARA’s approach to portfolio management places heavy emphasis on risk control.

Secondly, the ARA portfolios are by design very broadly diversified, to spread the risk across a great number of separate assets.

Thirdly, all the investments we make on behalf of our funds are held in safe custody by an independent third party of substantial means – in this case the National Australia Bank. This means the ownership and value of the investments remains intact regardless of what might happen to ARA. You never write a cheque to ARA for your investment dollar, and we never have any right or title over the assets of the investment funds.

ARA’s investment products carry no entry or exit costs whatsoever. All costs are quoted in the relevant Product Disclosure Statement, and will also be itemised in a personalised Statement of Advice provided to you before you commit to any investment.

ARA has developed the ARA Investment Fund and ARA Super for the use of its clients, and acts as the Investment Managed for the Funds, for which it is paid a fee. However, ARA has no affiliation whatsoever with any fund management group, bank, life insurance office or other financial institution, and receives no commissions or remuneration of any kind from the managers employed to manage any of the funds’ assets.

ARA provides quarterly statements for the ARA Investment Fund, and annual statements for ARA Super. In addition, we provide regular investment updates, along with other news bulletins at critical or newsworthy times.

We also run at least two client evenings a year to provide more detail, present wider views and take questions.

Investors can get current portfolio valuations by clicking “ARA Vault Login” in the top right hand corner of our website at any time.

Oh, and you can use the tried and true method of giving us a call and talking to the folks who run the shop.

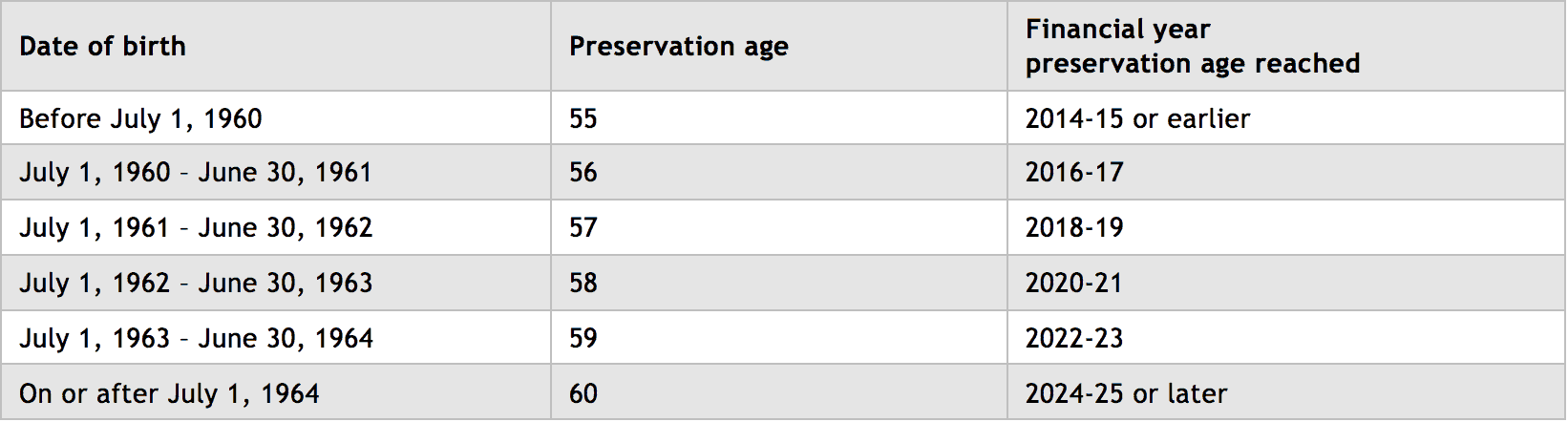

Legislation requires that money contributed to super is locked in until you retire or reach ‘preservation age’ – currently age 57, increasing gradually to age 60 as detailed in the table below. This is so except under severe hardship, death or permanent disability.

After preservation age you can access you super in full if you retire. If you continue working, you can access at least part of your super in the form of pension payments. Contact us for more information on your specific circumstances.

You are free to transfer your super between different providers at any time but beware of exit and entry costs they may have, and ensure you preserve any insurance entitlements. ARA Super carries no transaction costs at all.

Absolutely. ARA Super is a complying, public offer super fund and therefore eligible to receive contributions made by employers on behalf of their staff. And under Choice of Super legislation you are entitled to nominate to your employer the fund of your choice. Furthermore there may be significant cost savings to you by amalgamating the super you have received from different employers into the one fund.

The only exception is where, in certain circumstances, the award governing a particular job specifies which fund contributions are to go to. This is not a common situation.