This is the million dollar question – maybe literally! And a tough one to answer because there are so many moving parts. A whole range of issues that boil down to where, how well and for how long you want to live. Let’s give it a go.

It helps to think of this question in reverse. Think about how much income you will need to live the way you want to. You can then work back from that figure to calculate what amount of money you will need to support that requirement, or to test whether a given level of savings will cut the mustard.

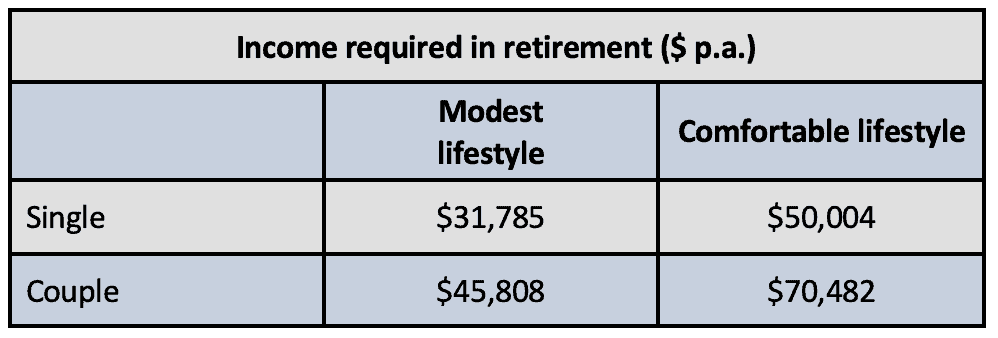

The Association of Superannuation Funds of Australia (ASFA) maintains a guide as to how much income singles and couples who own their homes require to provide for a “modest” and “comfortable” lifestyle.

This survey looks first at what retired Australians spend their money on, and then determines precise costs for those items. The results are then tested by selected groups of retirees for what looks reasonable and what does not.

The latest survey results available – as of March 2023 – for retirees around age 65 show as follows:

These are national average figures for 65-year olds. Figures for 85-year olds are lower, but not by much. The survey grapples with obvious subjective difficulties such as what constitutes “modest” and “comfortable”. But it does represent a valiant attempt to put a figure on a concept that can be very difficult to pin down.

The “modest” lifestyle is aimed at better than just survival on the Age Pension, but still assumes only basic activities. The “comfortable” lifestyle assumes an older, healthy retiree who:

- is involved in a range of leisure and recreational activities;

- runs a reasonable car;

- can update the kitchen or bathroom at some stage;

- entertains and eats out from time to time;

- purchases good quality clothing and household goods;

- maintains private health cover;

- can afford more frequent domestic (and occasional international) holidays.

You can see more at the ASFA website at www.superannuation.asn.au.

For reference, I note that the prevailing full rate of age pension is $27,664 for singles, $41,704 for couples. So the Age Pension amount is somewhat less than ASFA standard for even a modest lifestyle – which figures I guess in that its role is as a safety net.

Of course you can have other assets and income and still qualify for some Centrelink assistance. A single homeowner can have up to $280,000 in assessable assets (i.e. excluding the home) and still receive the full Age Pension, while a couple can have assets of $419,000. You can also earn some income from, say, part-time employment without affecting the pension.

Once assets reach the assets test threshold, the pension starts to reduce. So the additional income-earning potential from owning more assets is partially offset by the reducing eligibility for Age Pension. But we can have a go at estimating the amount of income you can expect to draw from the combination of your investments and the Age Pension, sustainably over the longer term. Bear in mind this is at best an estimate, and has to contend with a great many assumptions and uncertainties such as:

- What return will you actually achieve over several decades? It’s hard enough to predict what you’ll earn in a week, let alone 30 years;

- Will income demands reduce, stay the same or go up over the years? Conventional wisdom says spending reduces as you get older – although the ASFA survey says it’s not by much, and some expenses (eg medical costs) may well increase;

- Will the rules, particularly concerning Age Pension entitlement, get easier or tougher?;

- And of course, the Big One – how long will you live?

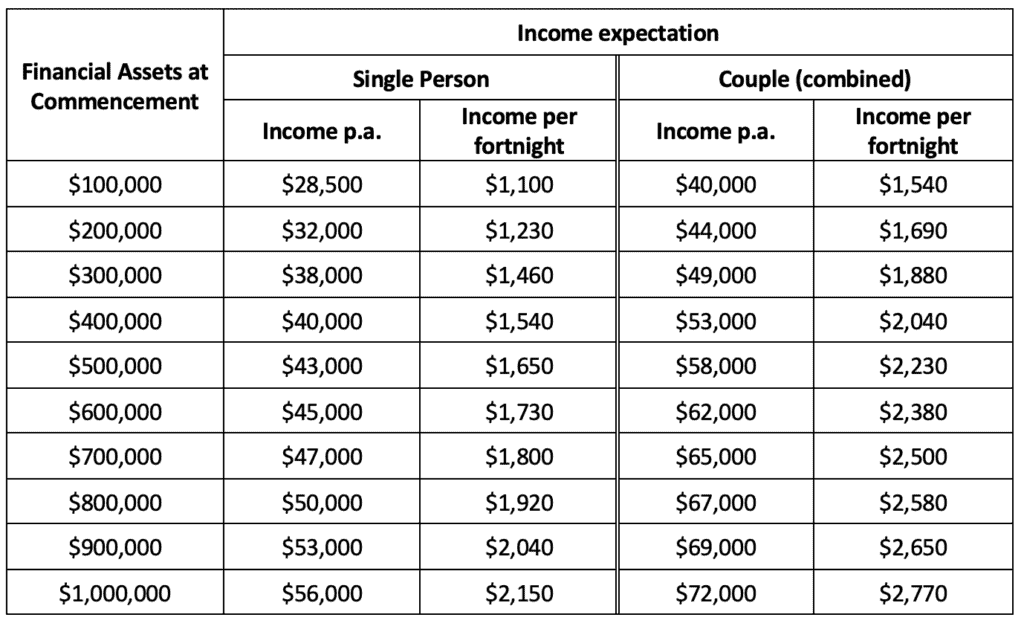

So take this as a well-meaning attempt to answer an impossible question. The numbers in the table below spell out the level of income that should be sustainable for a period of 30 years from age 65, including the Age Pension, based on having a certain level of financial assets that can be earning a return for you in retirement. The results assume:

- That you are a homeowner, and that a fire sale value of your personal effects, home contents and possessions is about $30,000. (For Centrelink’s purposes this is not unrealistic);

- Your portfolio is moderately conservative and earns on average between 5% and 5.5% per year;

- That annual income increases each year in line with inflation;

- That Centrelink’s eligibility rules remain close to what they are today.

At the risk of repetition, these income figures represent the income you could reasonably to expect to live on, including Centrelink entitlements where eligible, for a period of 30 years. At the end of that period the financial assets will have run out and you’ll be left with the Age Pension only.

You would cut back these income estimates if:

- You are sceptical as to the future availability of Age Pension benefits;

- You are planning on getting a telegram (or email or text message or hologram) from the King by living to 100 and beyond;

- You plan to eat out more as you get older (i.e. expenses will rise faster than the average).

Alternatively you could add to them if:

- You don’t mind drawing on the equity in your home. This will often happen in the normal course of events as retirees tend to sell the large family home and downsize in later years. Alternatively there is the reverse mortgage option offered by some banks, or Centrelink’s Pension Loans scheme;

- You expect living costs to reduce as you age;

- You are likely to do some part time paid work. I note that the means tests for Age Pension eligibility allow single pensioners to earn up to $190 per fortnight and couples to earn $336 per fortnight without impacting the Age Pension entitlement;

- You intend to age disgracefully, even if it means an early exit.

As it is, it seems that the Age Pension plus $200,000 invested gets a single retiree up to ASFA’s “Modest” lifestyle target, while almost $800,000 is needed to get to “Comfortable”. For couples, the nest egg required on top of the Age Pension is about $250,000 and almost $1,000,000 respectively.

A closer look at your personal circumstances might help unearth things that can tweak your personal outlook. Investment strategy and mix clearly have a direct impact, and it might be possible to safely improve the long term return using some prudent management techniques. Small changes to the underlying assumptions, indexation of income and the like can also make for a better result.

These numbers were estimated using our proprietary software package that allows us to consider changes in all the variables and assumptions listed, and to take into account tweaks of the investment strategy. We’d be happy to run some more numbers for you, and feel free to use the resources in our Retirement Hub.