Please 'Like' us on Facebook

Let’s keep this simple.

All it boils down to is how best to divvy up your savings ability among the options you have.

But what are those options? And which is best? Let’s take a look at each, and their pros and cons:

SUPERANNUATION

Super is the best game in town because, for most of us, it means paying the least amount of tax on our savings.

For all the details about why this is true, you can take a look at 5 Simple Steps to Understanding Super or read ‘RETIREASE’ but, for the moment, let’s accept that it’s true.

Super, however, is specifically designed for the sole purpose of providing for your retirement. So, your part of the deal for getting these very generous tax benefits is that you use the money for your retirement – and it’s locked away until then.

For those closer to retirement, that shouldn’t be a problem. But for younger people, chances are there are much more immediate calls on your money – like buying a house, sending the kids to school, and so on.

So, what else is there?

PAYING OFF DEBT

Debts like a housing loan, a credit card or a personal loan are usually not tax-deductible. So, in order to pay off that debt, you have to earn money, pay tax on it, and then clear the debt with what’s left after tax.

Let’s look at it another way:

It means that any money you put towards paying offnon-deductible debt can be said to earnwhatever the loan interest rate is – after tax.

So, if your home loan interest rate is 5%, and your personal tax rate is, say, 37%, then, effectively, the return on paying off that debt is as good as earning about 8% before tax.

Where else can you get a return like that – guaranteed and with no fees? And, for those debts with higher interest rates, like a credit card, it’s even better!

Chances are, the interest rate on your card is about 20%. If you don’t believe me, check your last statement. If your personal tax rate is 37%, then, effectively, the return on paying off your credit card is as good as earning about 31% before tax.

This means that clearing personal debts should be a highpriority. If you haven’t bought a house yet but intend to, save for it anyway to reduce the amount you’ll have to borrow. Think of it as pre-paying your mortgage.

Paying down personal debt makes sound economic sense, and it’s also good for the soul to keep the banks at bay.

NON-SUPER SAVINGS

This is everything else you can invest your money in. Term deposits, shares, property, managed funds and so on.

These are not as tax-effective as super, but at least they are accessible.

SO, WHAT’S THE RIGHT SPLIT?

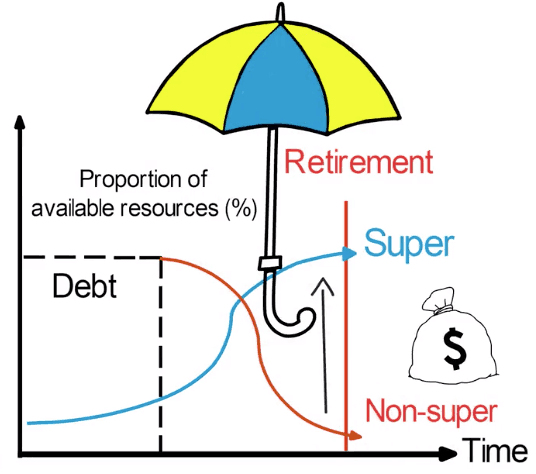

The chart below aims to summarise:

- The horizontal axis measures the time from now to retirement, and beyond.

- The vertical axis is the proportion of your available resources that you should allocate to each option.

- When you’re young and retirement is a long way off, put the minimum amount required into super. Concentrate on minimising your personal debt.

- Then, on that magical day when the debts are paid off, direct what you were using to pay off the debts towards some other form of saving.

- As you get closer to retirement, pay more and more attention to super contributions, and maybe even transfer some of your outside savings into super.

Last but not least, the umbrella. This is important. This is for the proverbial rainy day.

This whole plan is built around one thing – your ability to earn an income. If that stops for some reason – unemployment, illness, accident, or even death – the whole thing comes crashing down.

It is therefore extremely important to ensure that your plan is covered by adequate insurance of your income through life and income protection insurances, and that your beneficiaries are looked after by way of sound estate planning and a proper will.

And that’s it in a nutshell! Of course, the timing of these steps will vary from case to case, but these are the general principles to stick by.

Please 'Like' us on Facebook