Happy New Year everyone, best wishes for a safe and prosperous(!) 2019.

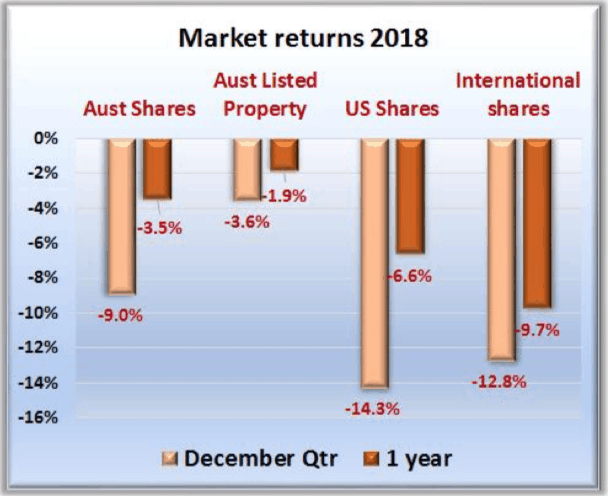

As far as the prosperous bit is concerned, 2018 turned out to be one of the tougher years. At the risk of understatement, investment markets and investor sentiment took a turn for the worse.

Hard going, particularly towards the end of the year. That is not an environment in which to expect stellar returns. Rather, the name of the game was capital preservation, and just staying in the black for the year was creditable. Holding plenty of cash made lots of sense.

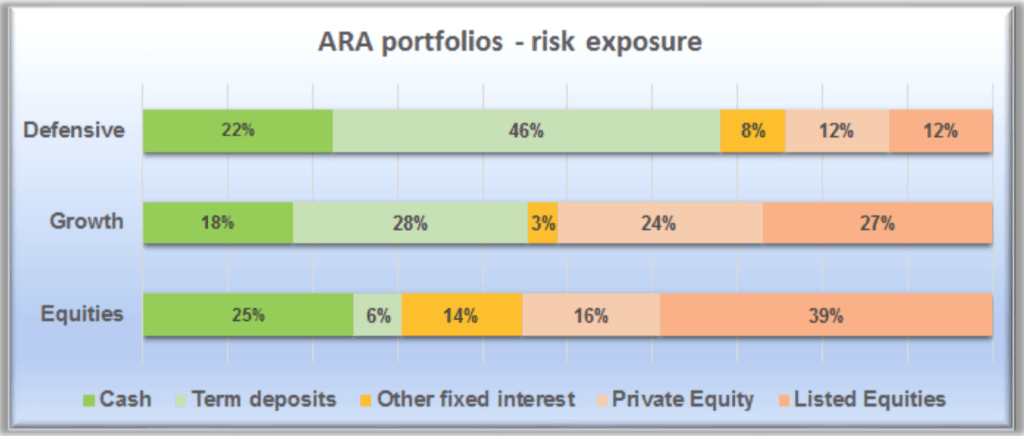

Indications are we could be in for more of the same in the new year, so we’re keeping plenty of powder dry. The tables on the following pages detail the funds’ holdings, and show that risk exposure remains low – lower even than at this time last year.

Having said that, market falls also create opportunity – to purchase or add to quality holdings at lower prices. So it’s equally important for investors not to let skittish markets scare them into inaction and miss the opportunity.

Looking at the tables of holdings, alert readers will note that a couple of old favourites have left the building. During the quarter successful exits from ProTen and Yumi’s were completed. Goodbye old friends, we’ll miss you. Some newbies have also appeared, so by way of introduction:

Pentalpha Income For Life

Pentalpha is a small but highly experienced team of fund managers managing a portfolio of mainly large companies listed on the Australian Stock Exchange. Their aim is to capture the strong stream of franked dividends while using options strategies to smooth the volatility in share prices.

It’s a philosophy that seems like a good match for risk-averse investors and is currently represented in the Defensive portfolio only.

Infradebt

Infradebt is a specialist infrastructure manager, primarily lending funds for specific projects, particularly those targeting:

• Renewable Energy

• Social Infrastructure, and

• Property, where there is an impact or environmental dimension.

This provides an attractive alternative fixed interest investment, currently in the Growth and Equities portfolios.

Future Generation Global

Future Generation Global is a listed investment company combining the skills of currently 14 different fund managers, none of whom charge the company management fees. This in turn allows the company to donate 1% of its assets to a variety of organisations, particularly in the fields of youth and mental health.

This is an effective way to gain diversified exposure to international share investing, while supporting worthy causes.

So, who’s got what?

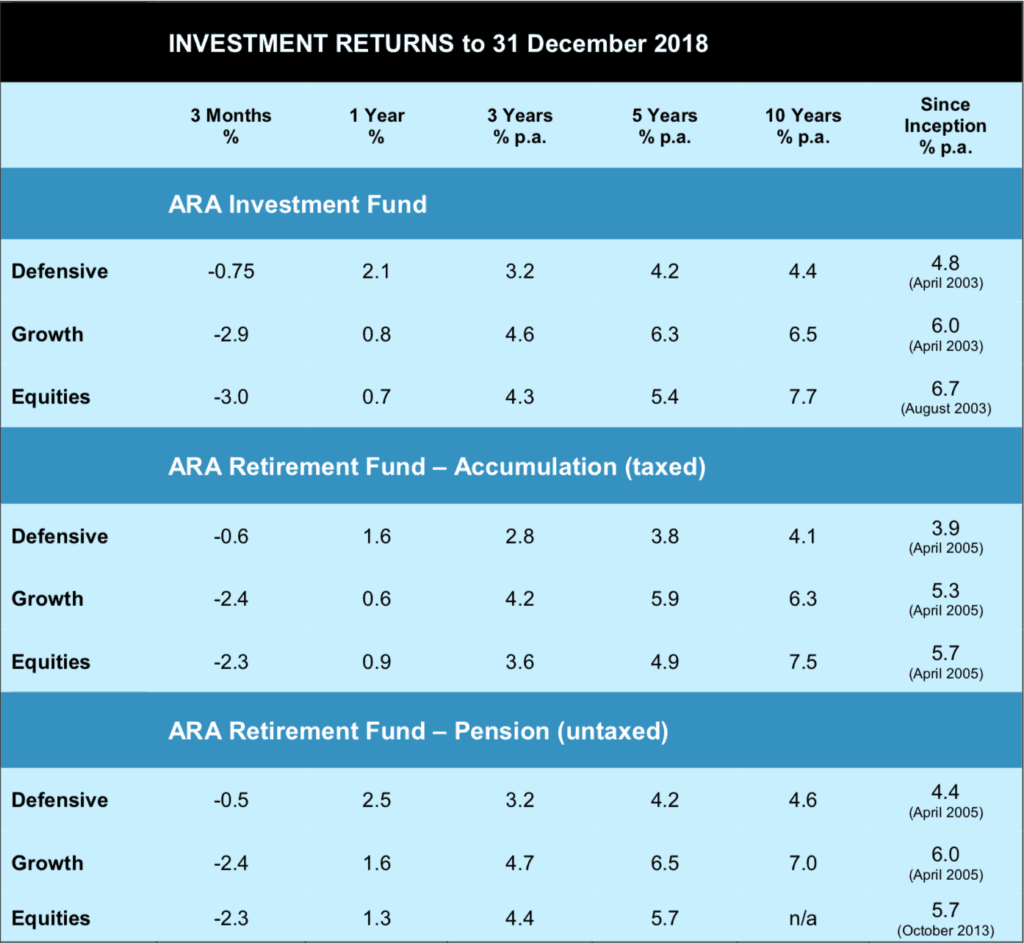

The table below shows the ARAIF’s investments as at the time of writing. Please note, the percentages refer to the proportion of each portfolio allocated to that investment, not its rate of return.

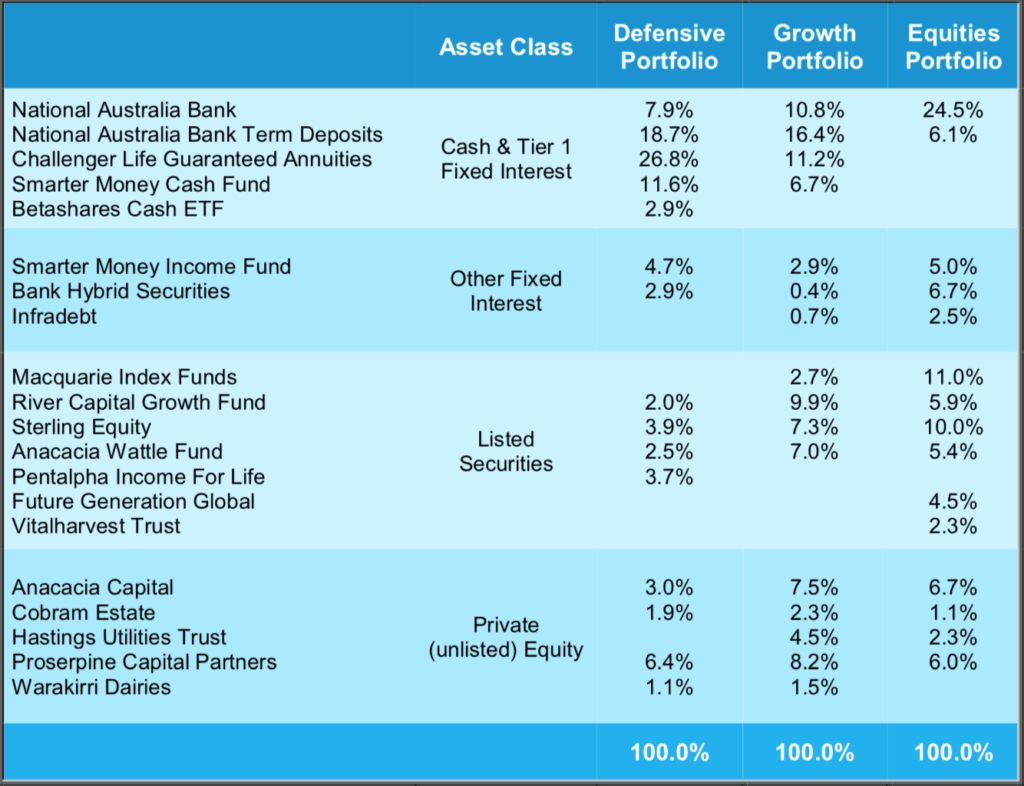

Major Holdings

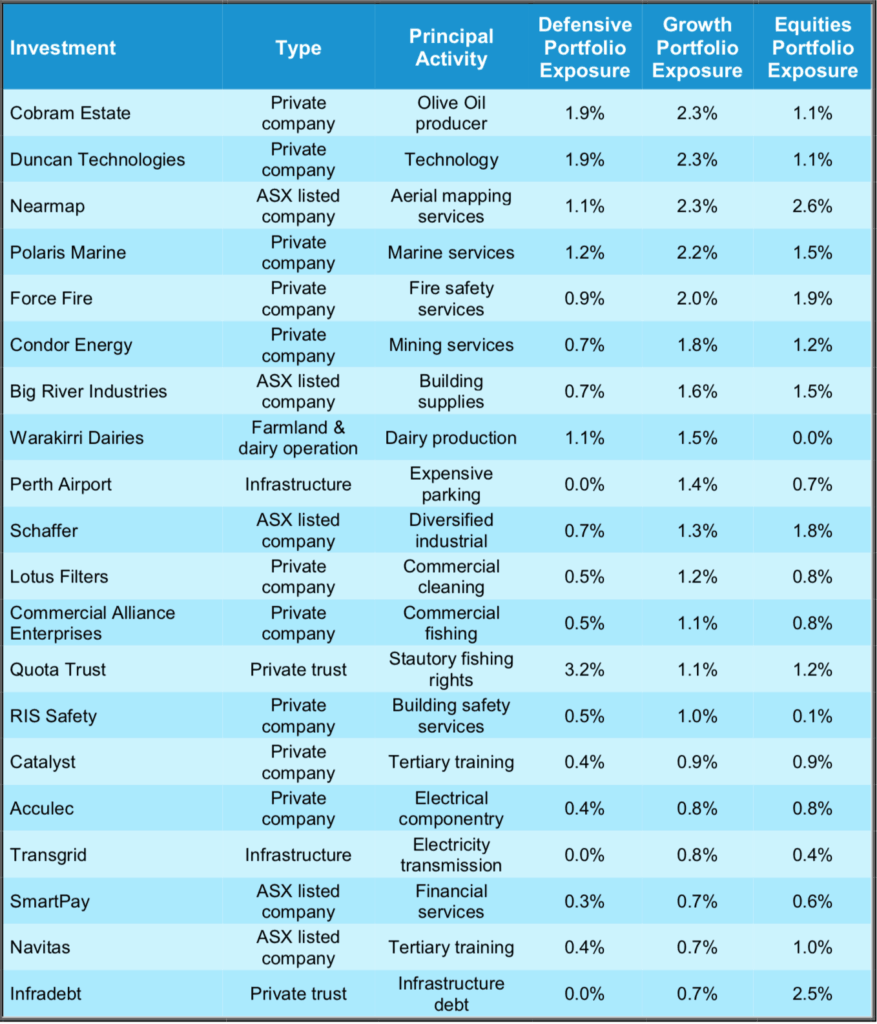

Apart from bank deposits and other interest-bearing accounts, the Fund invests in a range of assets through the fund managers listed in the table above. If we drill through to the assets selected and overseen by those managers, there are in fact over a hundred individual securities providing diversification of risk and exposure to a wide range of opportunities.

The table below shows the 20 largest individual holdings and what proportion of each portfolio they represent. These are the investments that will have the biggest impact on the return of your portfolio.

How come?

Given that even the Defensive portfolio had a small negative quarter, some clients have asked “If it’s holding so much cash, how come it drops at all?”

The answer is part mathematics, and partly the speed at which things happen.

Let’s say your cash and term deposits earn 4% per annum. It takes the whole twelve months to earn that 4%, which is 1% per quarter.

On the other hand, things like stock markets as we’ve seen can (and do) drop maybe 10% in a quarter.

So if 80% of your portfolio earns 1% for the quarter, and the other 20% drops 10%, your quarter result is:

(1% x 80%) – (10% x 20%) = minus 1.2% for the quarter.

The good news is that the reverse is also usually the case – that rebounds in your non- cash assets tend to happen quickly. Which works even better if you’ve topped up those assets when the prices were down.

What’s in a name?

At times like these it would seem particularly important that investors clearly understand what they are in, what their risks are, and what they can expect from their investment.

Unfortunately our industry persists in making things difficult in this regard.

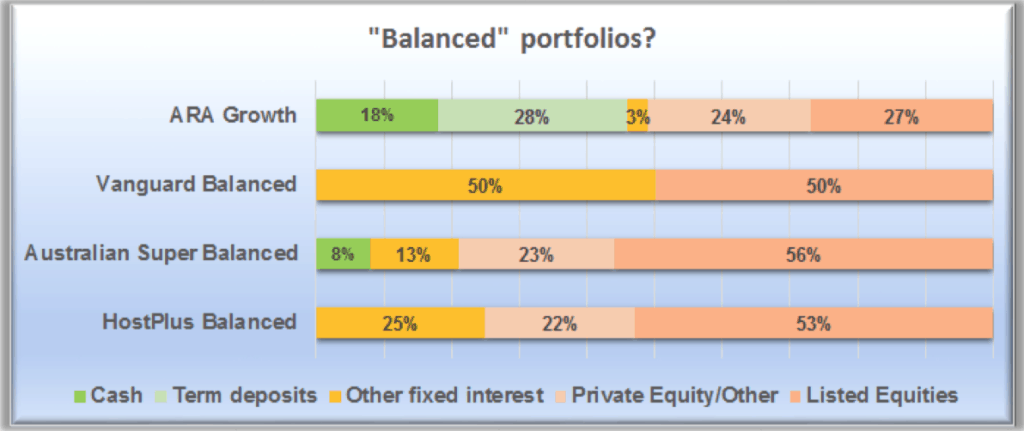

Take for instance the naming conventions (or lack thereof) for the various portfolio options from which investors can choose. Common among funds is the use of the term “Balanced”. Most (except maybe us) offer one by that name, but what is delivered can vary enormously.

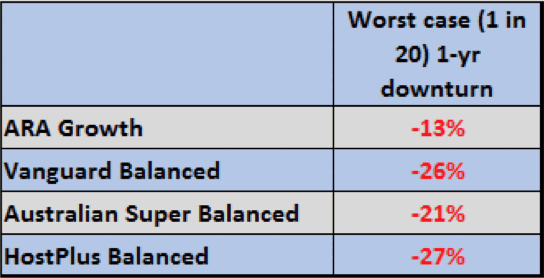

Let’s revisit the risk exposure chart from page 3, but show instead the Balanced options from a variety of major providers, compared in this case with our Growth portfolio.

Please understand it’s not our intention here to get all sanctimonious about who’s right and who’s wrong. Everyone has their own philosophyand methods and that’s fine. It’s just very clearthat there are widely varying approaches taking place under similar banners here, that will produce wildly different results in different sets of circumstances. Clearly the use of a certain moniker is no guide to the risks that investors take nor the results they can expect.

Our good friend Tim Farrelly, whose investment research we use and who wrote the article I have plagiarised drawn on for this one, proposes that a useful standard measure of risk would be how the portfolio would be expected to perform in a serious bear market. In fact Tim’s software enables us to do just that, a feature we have used extensively with clients and will continue to do so.

For the record, the programme estimates worst case 1-year returns in a 2008-type scenario for the respective portfolios as follows:

Sure, we had to make some assumptions to get to these results. They’re not foolproof, but intuitively the numbers would seem to provide a better indication or comparison of true underlying risk than generic portfolio labels.

What’s in store in 2019?

Remember when bank loans were hard to get? When you had to prove to the bank manager –typically a tough nut to crack – that you could actually repay it? Not just now but also if interest rates went up a couple of points. Because they do.

Then along came financial de-regulation and competition between banks, and borrowing became much easier. Governments (or at least their central banks) got into the act with extremely accommodating monetary policy – i.e. making lots of it available at historically miniscule interest rates. Even more so since the GFC, which was arguably caused by such easy money policies in the first place. All designed to encourage lending and spending, which keeps everyone happy – manufacturers, consumers, and therefore investment markets and investors.

Eventually though, the bank manager returns and wants his money back, and/or puts the interest rate up, which is exactly what’s happening. The US Federal Reserve is withdrawing funds from the system big time, banking regulation is tightening particularly here in Royal Commissionland, and interest rates are rising. All of which reduces what’s available to lend and spend. So everyone who was happy before isn’t so much any more – a fresh example being the previously unheard-of case of Apple downgrading its revenue forecast based on slowing sales particularly in China, leading to a 10% drop in its share price.

This is a long-winded way of saying that what have been the major drivers of investment markets over the past ten or twenty years are turning around. What worked before, like leveraging and passive buy-and-hold investment strategies, probably won’t looking ahead.

At the risk of – yet again – sounding like Mother Hen, it really is a time for caution. Be assured, we’ll continue to be careful with your hard-earned.