BETTER THINGS TO WORRY ABOUT

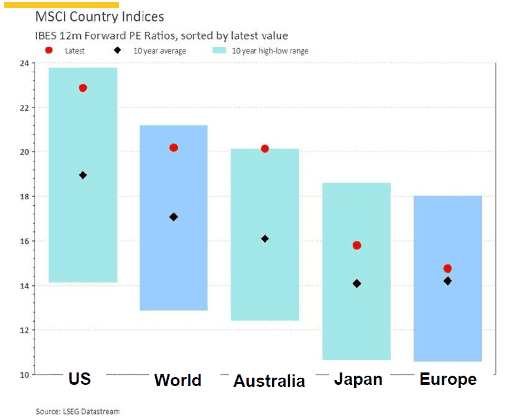

Alert readers may have pondered over the chart below from our last newsletter. It also got a run in our last round of Investor Updates. From feedback since, it seems a little more explanation might be in order.

Take the “Australia” bar for example. Stripped back, what it’s saying is that at different times over the past ten years, willing investors without a gun to their heads have been prepared to pay (or receive) a price that has varied between about $12 and $20 – for exactly the same thing!

That seems odd. $20 up from $12 is almost a 70% return – happy days. Conversely, falling from $20 to $12 is a 40% drop, which would have the journos scrounging for “crash” words.

Why does this happen? Well, that’s our system at work. Capitalism 101. The eternal struggle between greed and fear, optimism and pessimism, smart and dumb behaviour. The analysis adjusts for inflation, economic and profit performance and reflects only what investors will stump up at different times for a given investment.

Right now you’ll notice that the red dot is at the top end of the range, which means prices are very high, people are paying a lot, at least by historical comparison. The former head of the US Federal Reserve, Alan Greenspan, is credited with coining the term “irrational exuberance” to describe this phenomenon. Another writer, whose work I follow due to his slightly more pragmatic approach, calls it “Peak Stupidity”.

This cycle repeats over and over. There is absolutely nothing to suggest that the next ten years will be any different from the last ten. At some stage the red dot will head south – that is, market prices will fall. It might happen quickly, it might happen slowly. It might start next week, or in six years. There is no way of predicting exactly how or when it will unfold, only that it will.

So if you’re worried about a market downturn – don’t be. It will happen. It’s a sure thing, a much better bet than Half Yours was in the Melbourne Cup, although not as popular. Worrying about a sure thing is a waste of a good fret.

At times like this it’s tempting therefore to ask “Well, why not sell everything up and wait for the dust to settle?”.

That could be a tad drastic, given the expense (e.g. tax, transaction costs) and the fact that it might be years before it actually pays off. We already noted its unpredictability – no-one consistently gets that sort of timing dead right. Secondly, charts like this refer to the average of the entire market, the whole box and dice. So passive or “index” style funds are not meant to try – they are specifically designed to track the market average, for better- or worse. Very large institutional funds, thanks to their sheer bulk and the perceived competitive risk of being too different from the market average, either can’t or won’t.

And then – in case you hadn’t guessed – there’s us! A fundamental difference is that we operate primarily at the asset level, rather than trading on market averages. Our managers are continually evaluating each individual asset, comparing it against others so it’s competing for its place in the pool – regardless of what the average might be at the time. There is always something doing well, in spite of, rather than because of, market behaviour. And as we saw in the September update, there is a lot happening to keep the portfolios in appropriate shape for the time. So, no need to worry about that either.

Then why bother showing charts like that in the first place? Well, the problem, if you want to call it that, is when market averages do hit the skids, the press has a field day. The demands of the news cycle create a never-ending clamour for content, and a good old market crash is like Christmas for the journos. Bad news is infectious, and in that environment the daily valuations of everything, even quality assets, are likely to get caught up in the backwash.

Now that is only a problem if you are forced to sell at that time. If you can wait until the price recovers – no need to worry. At the risk of covering well-worn ground, our answer to that one is:

- Differentiate clearly between assets that will have price risk and those that won’t – only bank deposits and guaranteed annuities get into the second category;

- Ensure that each individual investor has enough of those secure assets to meet their unique set of cash needs for the foreseeable, plan-able future, without having to cash assets that might be prone to sentiment-driven price swings;

- Which leaves you free to devote the remainder of the portfolio to the higher returning assets that can get on with the long-term heavy lifting, unfussed by irrational, stupid market behaviour.

There’s enough out there to worry about already – no need to add your portfolio to the list.

ARA Consultants Pty Ltd provides this update for the information of its clients and associates. If you do not wish to receive this or other information about ARA in future, please contact us on (03) 9853 1688.